Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our each day e-newsletter, and/or observe us on Google Information!

In April 2025, the Worldwide Maritime Group did one thing uncommon for a UN physique: it handed a binding local weather coverage. Not advisory, not aspirational, however precise obligatory guidelines. The settlement commits worldwide delivery to net-zero greenhouse fuel emissions “by or round 2050,” and regardless of the paradox of that phrasing, the intent is evident. The business that accounts for roughly 3% of world CO₂ emissions is now formally on the clock. That’s not nothing. However earlier than we get away the low-sulfur champagne, it’s value unpacking what, precisely, this settlement commits to—and extra importantly, what it ignores.

The strengths of the IMO settlement are apparent if you happen to squint by the regulatory fog. It’s the primary international local weather mandate for a whole business. It features a international greenhouse fuel gasoline depth normal, phased in from 2027, and a two-tiered carbon pricing mechanism that may penalize ships for emissions exceeding their annual allotment. On the decrease tier, ships pay $100 per ton of CO₂ for average non-compliance. On the higher tier, that penalty jumps to $380 per ton. For a big vessel burning 100 tons of gasoline per day and emitting roughly 3.1 tons of CO₂ per ton, that’s over $117,000 in fines per day of operation in the event that they’re considerably over the benchmark. Over a 20-day trans-Pacific voyage, you’re staring down greater than $2 million in carbon prices. That’s not a rounding error.

However the weaknesses are simply as plain. The 2030 goal—a 20% to 30% discount in absolute emissions—is unlikely to be met, even with these guidelines, as a result of the carbon pricing doesn’t chunk till 2028. The settlement provides ships one other three years of business-as-usual, exactly when cuts are most pressing.

Worse, the trail to 2040 is a thriller. The present construction ends with 2035 gasoline depth targets, and the subsequent algorithm gained’t be determined till 2032. Which means the trajectory to 70% emissions discount by 2040 is predicated on coverage that doesn’t but exist.

And naturally, the present four-year model of the USA walked out. The identical nation that was as soon as pushing the IMO for stronger targets abruptly reversed course, reportedly calling the carbon levy “unfair to American delivery.” That’s wealthy, contemplating the U.S. barely has any worldwide flag carriers left to be taxed and makes fewer business ships than both tiny Norway or fashion- and wine-giant Italy yearly. The mixture of the Jones Act, a fetishization of unregulated markets and nil curiosity in industrial insurance policies for 45 years has led to the USA, as soon as the most important ship constructing nation on the planet, largely constructing a number of very, very costly army ships.

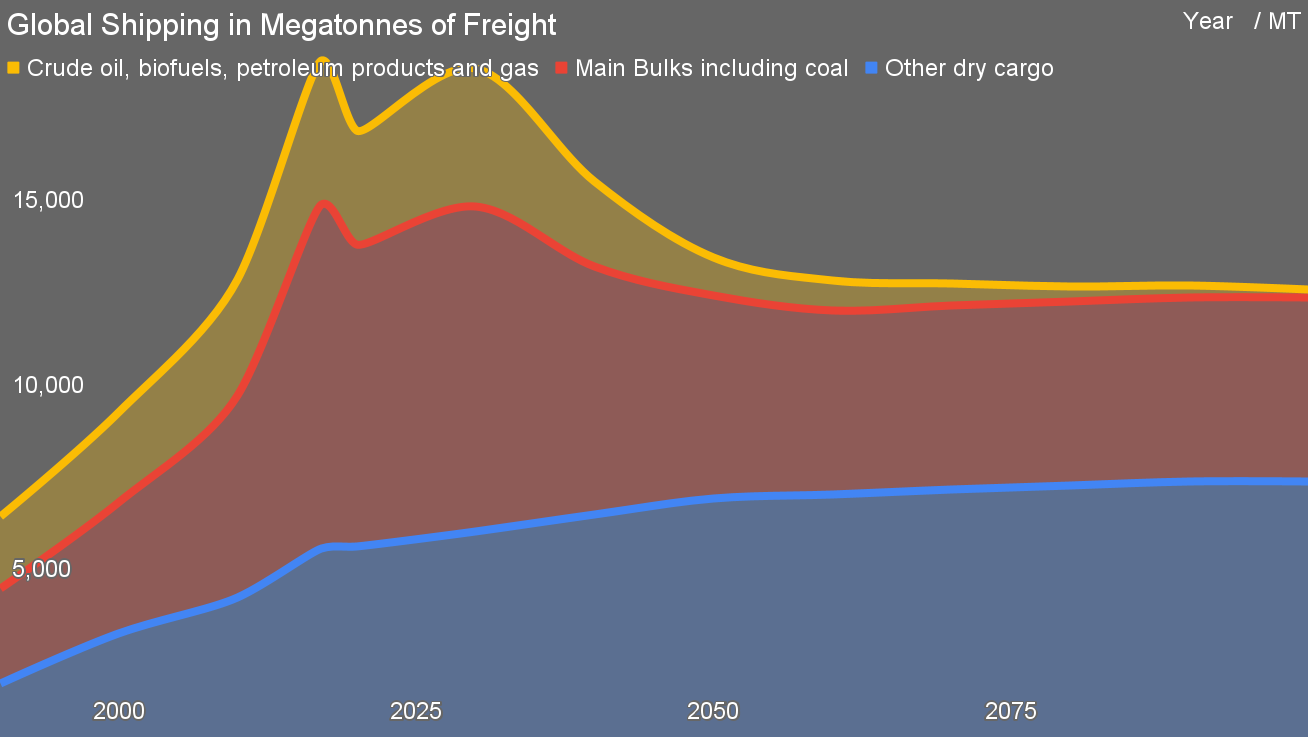

What the IMO settlement fails to mirror is that the issue it’s making an attempt to resolve is shrinking. It’s primarily based on legacy assumptions that delivery demand will proceed to rise consistent with international GDP, and that the one approach to take care of emissions is to swap out fuels whereas conserving fleet dimension and cargo volumes fixed. Their modeling is predicated on 40 or so individuals who apparently by no means heard of local weather change projecting delivery volumes into the longer term primarily based on 1990 to 2019 numbers. However that’s not what the real-world decarbonization trajectory appears like.

Probably the most primary truth the IMO, or no less than its most well-liked supply materials, doesn’t account for is that international commerce in fossil fuels makes up almost 40% of all seaborne tonnage. Coal, oil, fuel—these aren’t simply massive emitters when burned; they’re massive shippers. And in a decarbonizing world, they go away. Coal delivery collapses first, already down in key markets. Oil demand peaks within the 2020s. LNG persists longer however nonetheless declines earlier than mid-century. That alone wipes out 40% of maritime quantity. And that’s earlier than contemplating the 15% of delivery presently dedicated to iron ore, a lot of which turns into out of date when China stops constructing infrastructure and nations begin making metal from recycled scrap in electrical arc furnaces positioned close to demand.

The IMO’s projection? Doubling of bulks by 2050. Nevertheless, their goal is zero earlier than my projection will get there. Aggression is sweet typically.

If you strip out the declining fossil cargo, change to electrified inland and coastal delivery, and introduce modest effectivity enhancements, the remaining deep-sea delivery downside shrinks quick. In my 2022 projection, I estimated that by 2100, delivery emissions would plummet with out counting on artificial fuels or radical redesigns—simply by declining fossil commerce, electrification of sub-1,000 km routes, and a rational power transition. The IMO, in distinction, has designed a zero-carbon regulatory equipment to resolve an issue multiples of the dimensions of what’s going to truly exist by mid-century. It’s planning to switch all bunker gasoline, when in reality loads of that demand goes away.

Which brings us to the answer that truly suits the dimensions of the remaining downside. If the aim is to decarbonize the remaining deep-water cargo routes, masking voyages longer than 2,000 km and vessels over 5,000 gross tons, the IMO settlement restrict, then you definately don’t want e-methanol or ammonia for each ship. You want a battery on board, a tank of biodiesel, and a few math. Let’s run it.

Begin with the port and nearshore segments. For environmental and regulatory causes, these are the zones most urgently in want of zero-emissions operation. A 200 nautical mile stretch from shore in every course, 400 NM whole, is sufficient to cowl emission management areas (ECAs), port maneuvering, and loading and unloading home windows. ECAs are zones designated by the IMO the place ships should meet stricter limits on sulfur, nitrogen oxides, and particulate emissions to guard coastal air high quality. There are presently 4 ECAs: the Baltic Sea, the North Sea, North America, and the U.S. Caribbean.

For a 5,000+ ton vessel utilizing about 2.4 MWh per NM, you want roughly 960 MWh of battery capability. At 300 Wh/kg LFP cells, that’s a battery weighing 3,200 metric tons. On a 60,000 DWT containership, that’s about 5% of payload. It’s a tradeoff, however not a dealbreaker. At $65/kWh, the most recent LPF BESS worth out of China’s auctions , the complete battery prices ~$60 million. Assuming a 3,000-cycle life, it may be amortized over a 30-year vessel lifetime and contribute lower than $20 per MWh delivered. The electrical energy to cost it at port? In international locations with clear grids or devoted renewables, determine $0.10/kWh, or ~$100,000 per voyage phase. Complete nearshore power price: lower than $300,000 per voyage. Zero native air pollution. Zero carbon emissions. Zero future retrofit price.

For the remaining 3,400 NM on a trans-Atlantic or 6,100 NM on a trans-Pacific route, the battery isn’t going to chop it. That’s the place the gasoline is available in. However it doesn’t must be ammonia or e-methanol. It doesn’t even must be fancy. It simply must be biodiesel. At 42 MJ/kg and roughly 85% decrease lifecycle GHG emissions than fossil marine gasoil, HVO biodiesel does the job. A ship burning 1,600 tons of biodiesel for the Atlantic or 2,900 tons for the Pacific pays about $1,100 per ton, or $1.8 to $3.2 million per journey. That’s greater than fossil gasoline, however not dramatically so—and it avoids $1.5 to $2.8 million in carbon fines at $380 per ton of CO₂. Higher but, it doesn’t require engine alternative, retrofitted bunkering tanks, or a multi-decade port gasoline transition plan. It simply goes in the identical tank as earlier than.

Biomethanol prices extra, however could also be required just because—as chemical course of engineer and plant designer Paul Martin factors out after we talk about this—the molecules matter, and the molecules in biodiesel are considerably restricted, arduous to make and completely required for lengthy haul aviation. The numbers might crunch out to biomethanol being what results in a lot larger gasoline tanks for crossing oceans. Greater as a result of methanol has 45% the power density of present bunker fuels.

Artificial methanol, against this, prices about $1,400 per ton, and that power density bites arduous. For a similar 6,100 NM trans-Pacific crossing, that’s 5,300 tons of gasoline, or $7.4 million. You save the carbon penalty, positive, however you continue to pay greater than double the biodiesel hybrid. Inexperienced ammonia is even worse: you want over 5,700 tons of gasoline for a similar journey, at $1,000 per ton, and also you additionally want cryogenic or pressurized tanks, new combustion tech, and security techniques for a gasoline that’s poisonous, corrosive, and flammable in all of the unsuitable methods. Ammonia’s solely benefit is that it doesn’t include carbon. However neither does logic, and logic says you don’t carry round thrice the amount of a gasoline that may kill the crew if you happen to don’t need to.

What the IMO must do now’s match coverage to physics. The delivery sector shouldn’t be going to decarbonize on a one-size-fits-all molecule. It’s going to decarbonize on fewer ships, fewer kilometers, and fewer tons of gasoline. Most short-sea delivery will go electrical. Inland delivery already is. Fossil cargo will vanish. Commerce will regionalize. The long-haul delivery sector will shrink. And what stays could be served by batteries and biofuels for nearly all journeys. That’s the map. Anything is drawing zero-carbon traces on an evaporating ocean.

Whether or not you might have solar energy or not, please full our newest solar energy survey.

Have a tip for CleanTechnica? Need to promote? Need to counsel a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our each day e-newsletter for 15 new cleantech tales a day. Or join our weekly one if each day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage

{kind=link}