Assist CleanTechnica’s work by means of a Substack subscription or on Stripe.

Cross laminated timber is commonly introduced as a housing resolution, a method to construct sooner and extra affordably whereas decreasing the carbon locked into buildings. That’s true, however it’s also half of a bigger story concerning the heavy supplies industries. Each time a cubic meter of cross laminated timber (CLT) replaces concrete, the demand for cement and the demand for rebar decline. Over a long time, these substitutions add up. What seems to be like a small shift in development strategies on the challenge stage turns into a driver of world demand curves for each cement and metal. By bending these curves downward, CLT helps make decarbonization within the heaviest industries extra practical.

The primary three articles on this sequence established the muse. The opening piece confirmed that CLT and modular development are Canada’s quickest lever to handle the housing scarcity and embodied emissions on the identical time. The second article explored Mark Carney’s Construct Canada Houses initiative and argued that authorities should act as an anchor buyer for CLT factories, turning coverage into actual sq. footage. The third article laid out the mass timber playbook, describing the necessity to combine sawmills, bioenergy, adhesives, and logistics right into a coherent worth chain. This text builds on that basis by trying outward, asking how CLT shapes the long run trajectories of cement and metal demand.

For years, projections of cement and metal demand have assumed nearly linear progress according to GDP and urbanization. These fashions usually level to mid-century peaks and flat demand effectively into the again half of the century. My evaluation is totally different. The Chinese language infrastructure and constructing growth that drove international demand within the final twenty years has peaked. Superior economies are shifting from enlargement to upkeep. Effectivity good points are actual and accelerating. Substitution pressures from timber, light-weight composites, and smarter design are beginning to chunk. Taken collectively, the result’s that international demand for each cement and metal will peak earlier, flatten extra shortly, after which decline regularly for the remainder of the century.

Cement is the clearest instance. In mid-rise residential and components of the business sector, CLT is already displacing concrete slabs and cores. Codes are evolving to permit taller timber buildings and procurement insurance policies are beginning to acknowledge embodied carbon. Supplementary cementitious supplies are being blended into mixes around the globe, decreasing the clinker ratio in each cubic meter of concrete.

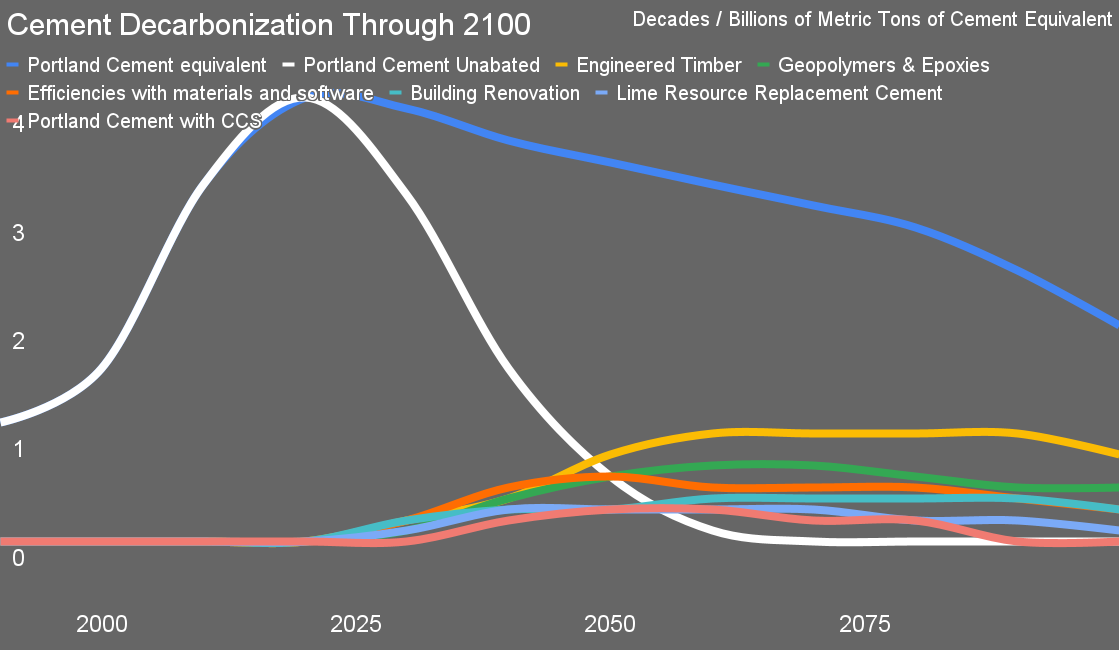

In my projection curves, cement demand doesn’t climb steadily to 2100. It peaks within the 2020s, flattens within the 2030s, after which declines to a few third of in the present day’s ranges by the tip of the century. The drivers are substitution by mass timber the place it is smart, effectivity in design that makes use of much less materials, and caps on embodied carbon that reward decrease carbon options. The cuts chunk hardest in residential and workplace buildings, the place modular CLT is changing into a mainstream possibility. Infrastructure like highways and dams will proceed to want cement, however the combination volumes won’t offset the reductions within the constructing sector.

In its long-term forecast, the World Cement Affiliation agrees that international cement demand, notably for clinker, will peak effectively earlier than mid-century after which decline considerably. The white paper means that demand might fall from round 4.2 billion tons in 2020 to roughly 3.0 billion tons by 2050. By mid-century, cement demand might sit at simply half of in the present day’s stage, pushed by slower progress in China, expanded use of substitutes and design efficiencies, and the rise of low-carbon options. That outlook aligns carefully with my modeling. The place most forecasts anticipate continuous progress, WCA sees a future reshaped by materials substitution and effectivity, precisely what mass timber brings to the desk.

As a facet notice, this is among the few instances the place my projections of demand decline in main industries is publicly agreed on by the business itself. There are financial causes for a public projection of progress even when the business is aware of it’s going through decline or at minimal a lot slower progress. Take a look at oil and fuel, maritime transport, and aviation for prime examples, in addition to the absurd projections of hydrogen demand progress.

Metal is tied carefully to cement as a result of a lot metal goes into rebar and structural frameworks for concrete buildings. As concrete declines, so does the necessity for rebar. My projections present international metal demand bending downward in parallel with cement. This doesn’t imply metal vanishes. Infrastructure, automobiles, and equipment will proceed to require it, however the rebar section will shrink steadily. The chance that comes with this shift is important. A flatter and declining metal demand curve makes it attainable for electrical arc furnaces powered by clear electrical energy to dominate international manufacturing. That transition is dependent upon scrap flows being ample to cowl a bigger share of demand.

With decrease complete demand, the scrap accessible is sufficient to feed extra of the system. In impact, the substitution of CLT for concrete not solely cuts emissions straight but in addition makes the metal business’s decarbonization drawback simpler by decreasing volumes and aligning with scrap based mostly pathways.

The guiding coverage that emerges from this evaluation is evident. We should always prioritize timber in buildings the place it performs as effectively or higher than concrete and metal, and codes and financing ought to favor low embodied carbon supplies. Procurement ought to credit score the biogenic storage in timber, recognizing the carbon locked away in panels for many years. Embodied carbon caps in constructing codes can nudge builders and designers towards supplies that rating higher on life cycle evaluation. These aren’t radical steps. They’re sensible instruments that reward higher selections and speed up substitution.

The actions are equally concrete. Timber ought to grow to be the default for multi-unit residential buildings and mid-rise workplaces. Hybrid designs ought to change podiums, stairwells, and cores with timber the place engineering helps it. Cement mixes needs to be pushed towards most supplementary content material, reducing clinker volumes wherever attainable. Metal producers ought to double down on electrical arc furnace pathways, aligning recycling infrastructure and scrap assortment with projected demand. Taken collectively, these steps lock within the displacement of cement and metal within the constructing sector and make the heavy business decarbonization problem manageable.

Dangers stay. If codes evolve too slowly, substitution will lag. If insurance coverage markets resist, adoption can be slower. Incumbent industries will proceed to defend their markets. Lumber provide volatility and land administration controversies can undermine the case for mass timber if not dealt with responsibly. On the identical time, the enablers are robust. CLT prices are coming down with scale. Authorities procurement can lead by instance. Traders are specializing in embodied carbon as a part of ESG mandates. Export markets, notably in america and Europe, are opening shortly to mass timber options.

The conclusion is that CLT is among the sharpest knives we now have to chop into international cement and metal demand, decreasing the challenges of coping with emissions from these hard-to-abate sectors. It isn’t the one lever, however it’s a highly effective one which compounds over a long time. By displacing concrete and the rebar inside it, CLT bends each curves downward, turning what appeared like an not possible decarbonization climb for heavy business right into a slope that may be managed.

My projections for cement and metal by means of 2100 mirror this actuality. Cement peaks quickly, declines steadily, and ends the century at a few third of in the present day’s ranges. Metal flattens, declines, and transitions to an electrical arc furnace dominant business powered by clear electrical energy and ample scrap. These curves aren’t simply numbers. They’re pathways to aligning housing, financial system, and local weather in a method that makes the longer term much less daunting and extra achievable.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive stage summaries, join our every day e-newsletter, and comply with us on Google Information!

Have a tip for CleanTechnica? Wish to promote? Wish to recommend a visitor for our CleanTech Speak podcast? Contact us right here.

Join our every day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if every day is just too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage

{kind=link}