Emissions goal setting amongst America’s largest firms exhibits restricted indicators of enchancment — and one key metric has declined.

That’s based on researchers on the College of California, Los Angeles, who reviewed sustainability studies, local weather transition plans and different materials from 2023 for S&P 500 firms, which collectively make up round 80 % of the worth of the U.S. market.

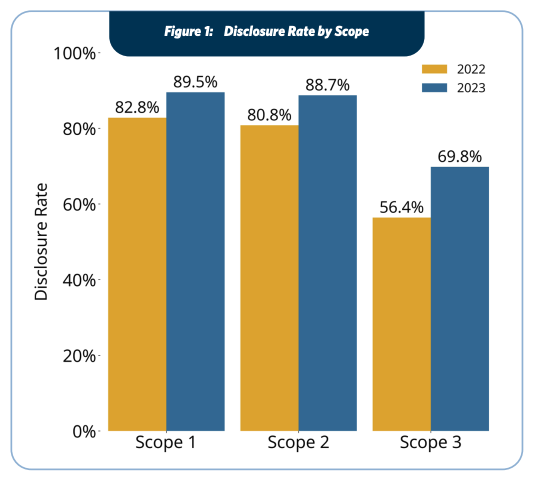

Trying up: Disclosure

Disclosure of Scopes 1 and a pair of is changing into uniform and Scope 3, the place disclosure charges have traditionally been a lot decrease, is catching up.

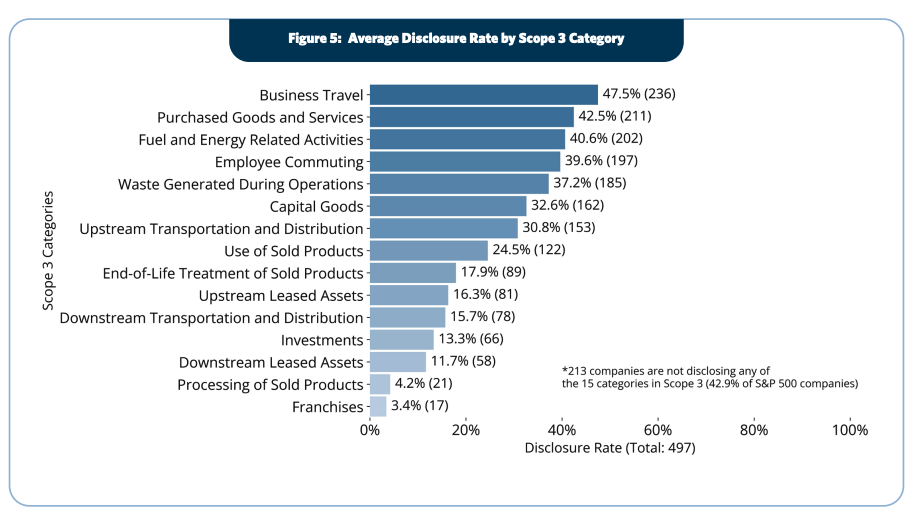

However the headline quantity for Scope 3 hides inconsistent reporting throughout the 15 totally different classes of emissions that make up the scope.

The deal with enterprise journey — Scope 3 Class 6 — is probably going as a result of the info is comparatively simple to gather, recommended the UCLA staff, which was led by Magali Delmas, a professor of administration. “Class 6 represents simply 12.5 % of total reported Scope 3 emissions,” the researchers famous, “highlighting a transparent disconnect between ease of reporting and emissions significance.”

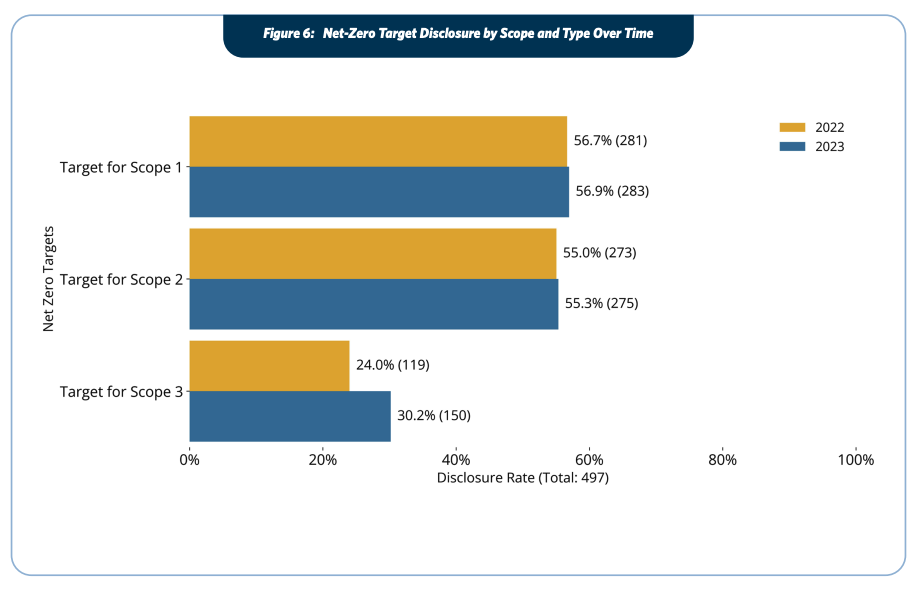

Going nowhere: Goal setting

Disclosure is meant to be a primary step towards setting and implementing targets for emissions reductions. And in terms of internet zero targets, progress on Scope 3 additionally stays stable, however motion on Scopes 1 and a pair of has all however stalled.

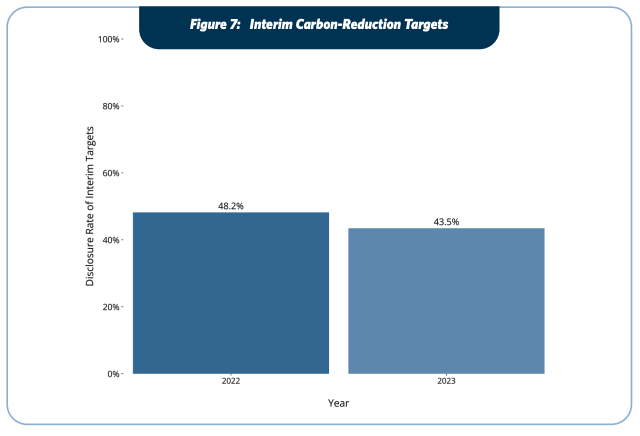

Web zero commitments usually have a goal yr between 2040 and 2050. To make sure that firms don’t delay taking motion, customary setters such because the Science Primarily based Targets initiative require firms to set interim objectives, typically for 2030. However the variety of firms doing so declined between 2022 and 2023.

“That is worrisome,” the report famous, “as these near-term objectives are essential for monitoring progress and figuring out emission-reduction alternatives.”

The UCLA research is certainly one of a number of from the previous yr to have checked out disclosure and goal setting within the personal sector, together with a PwC survey, which painted a broadly constructive of company motion, and one other from Accenture, which surfaced extra combined outcomes. The outcomes aren’t essentially contradictory, partially as a result of every research checked out a unique pattern of firms: PwC surveyed disclosures made by CDP by 7,000 firms and Accenture regarded on the largest 2,000 firms by income.

{kind=link}