The success of machine studying pipelines is determined by characteristic engineering as their important basis. The 2 strongest strategies for dealing with time sequence knowledge are lag options and rolling options, in response to your superior methods. The power to make use of these methods will improve your mannequin efficiency for gross sales forecasting, inventory worth prediction, and demand planning duties.

This information explains lag and rolling options by exhibiting their significance and offering Python implementation strategies and potential implementation challenges by means of working code examples.

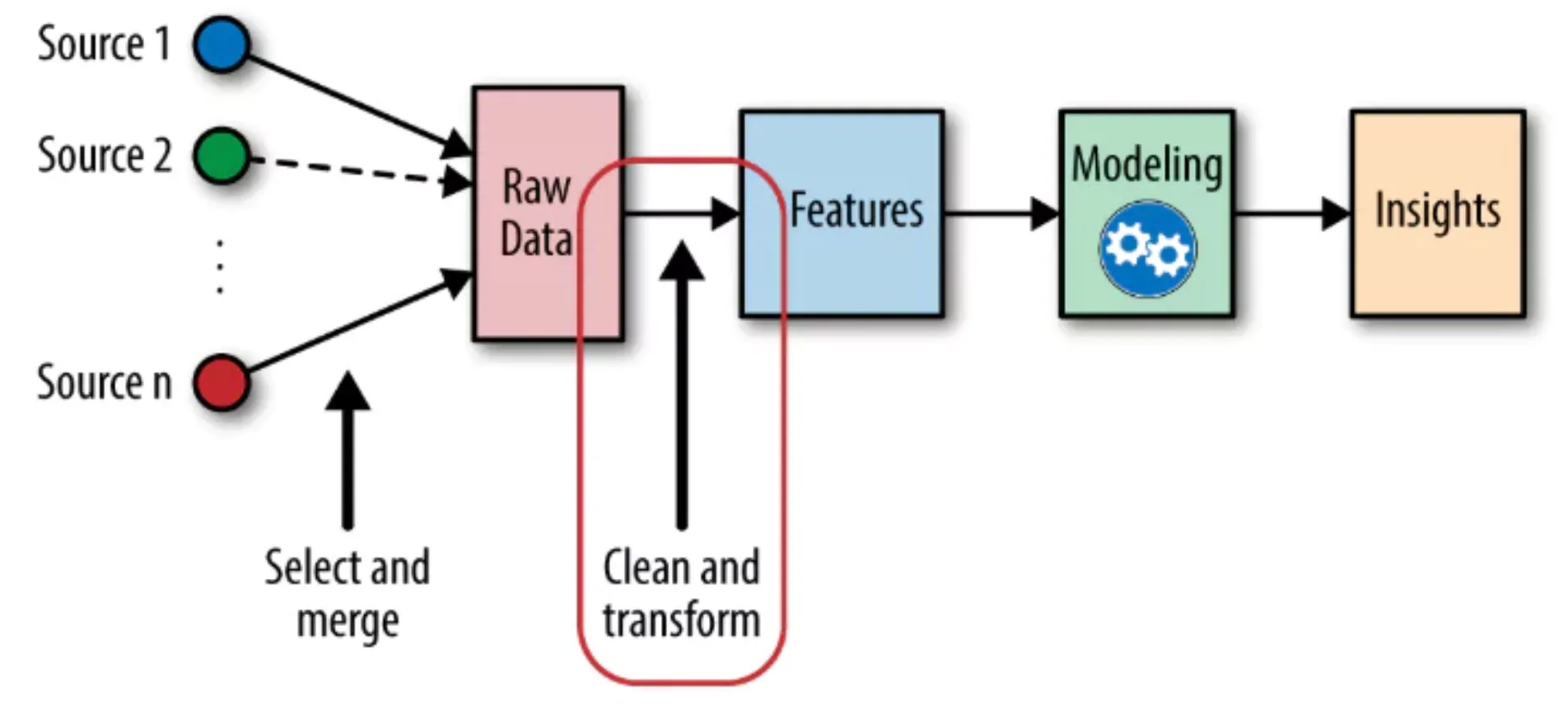

What’s Characteristic Engineering in Time Collection?

Time sequence characteristic engineering creates new enter variables by means of the method of reworking uncooked temporal knowledge into options that allow machine studying fashions to detect temporal patterns extra successfully. Time sequence knowledge differs from static datasets as a result of it maintains a sequential construction, which requires observers to grasp that previous observations influence what is going to come subsequent.

The standard machine studying fashions XGBoost, LightGBM, and Random Forests lack built-in capabilities to course of time. The system requires particular indicators that want to indicate previous occasions that occurred earlier than. The implementation of lag options along with rolling options serves this goal.

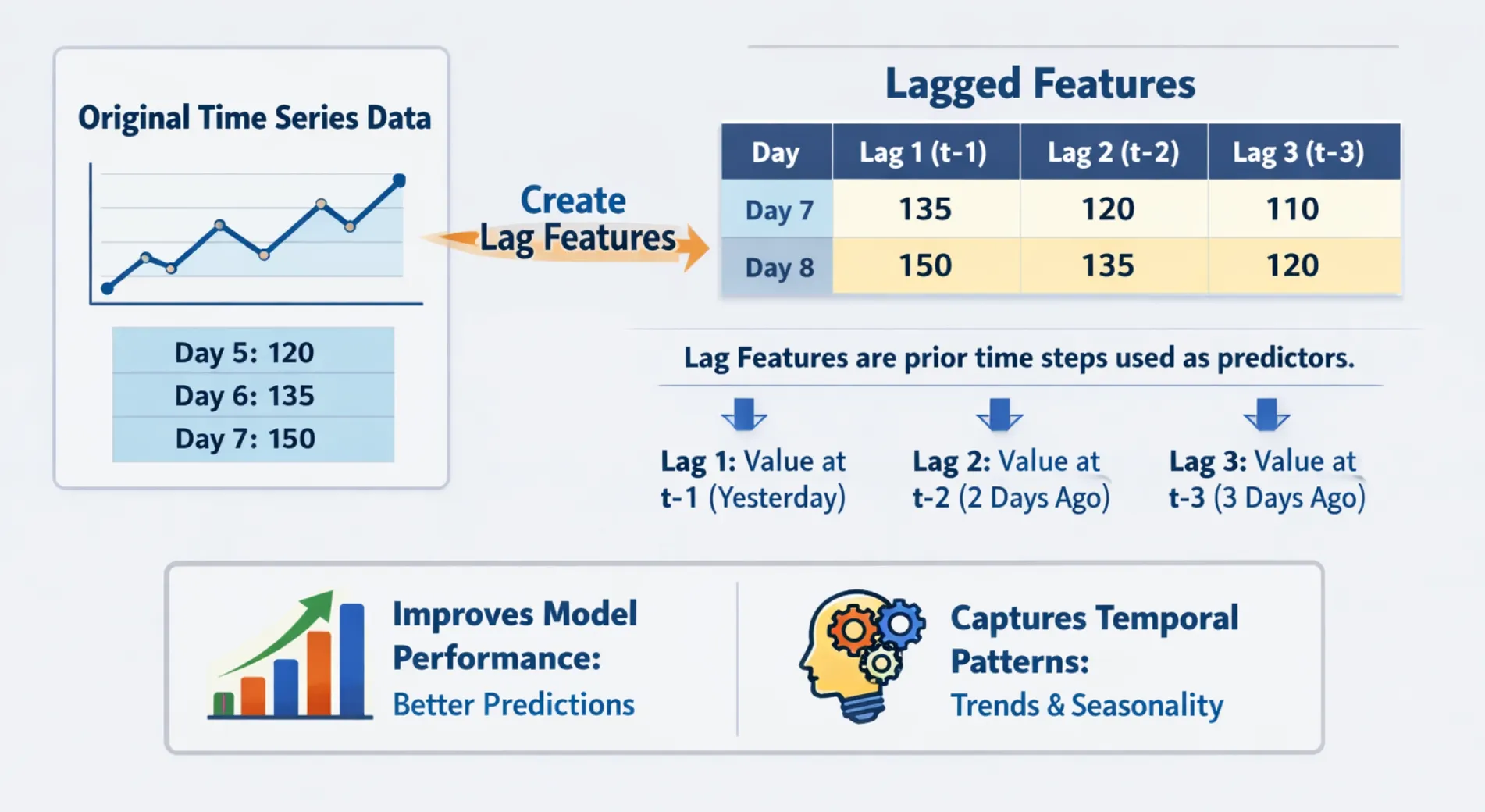

What Are Lag Options?

A lag characteristic is solely a previous worth of a variable that has been shifted ahead in time till it matches the present knowledge level. The gross sales prediction for right this moment is determined by three completely different gross sales info sources, which embody yesterday’s gross sales knowledge and each seven-day and thirty-day gross sales knowledge.

Why Lag Options Matter

- They characterize the connection between completely different time durations when a variable exhibits its previous values.

- The tactic permits seasonal and cyclical patterns to be encoded with no need difficult transformations.

- The tactic gives easy computation along with clear outcomes.

- The system works with all machine studying fashions that use tree constructions and linear strategies.

Implementing LAG Options in Python

import pandas as pd

import numpy as np

# Create a pattern time sequence dataset

np.random.seed(42)

dates = pd.date_range(begin="2024-01-01", durations=15, freq='D')

gross sales = [200, 215, 198, 230, 245, 210, 225, 260, 275, 240, 255, 290, 305, 270, 285]

df = pd.DataFrame({'date': dates, 'gross sales': gross sales})

df.set_index('date', inplace=True)

# Create lag options

df['lag_1'] = df['sales'].shift(1)

df['lag_3'] = df['sales'].shift(3)

df['lag_7'] = df['sales'].shift(7)

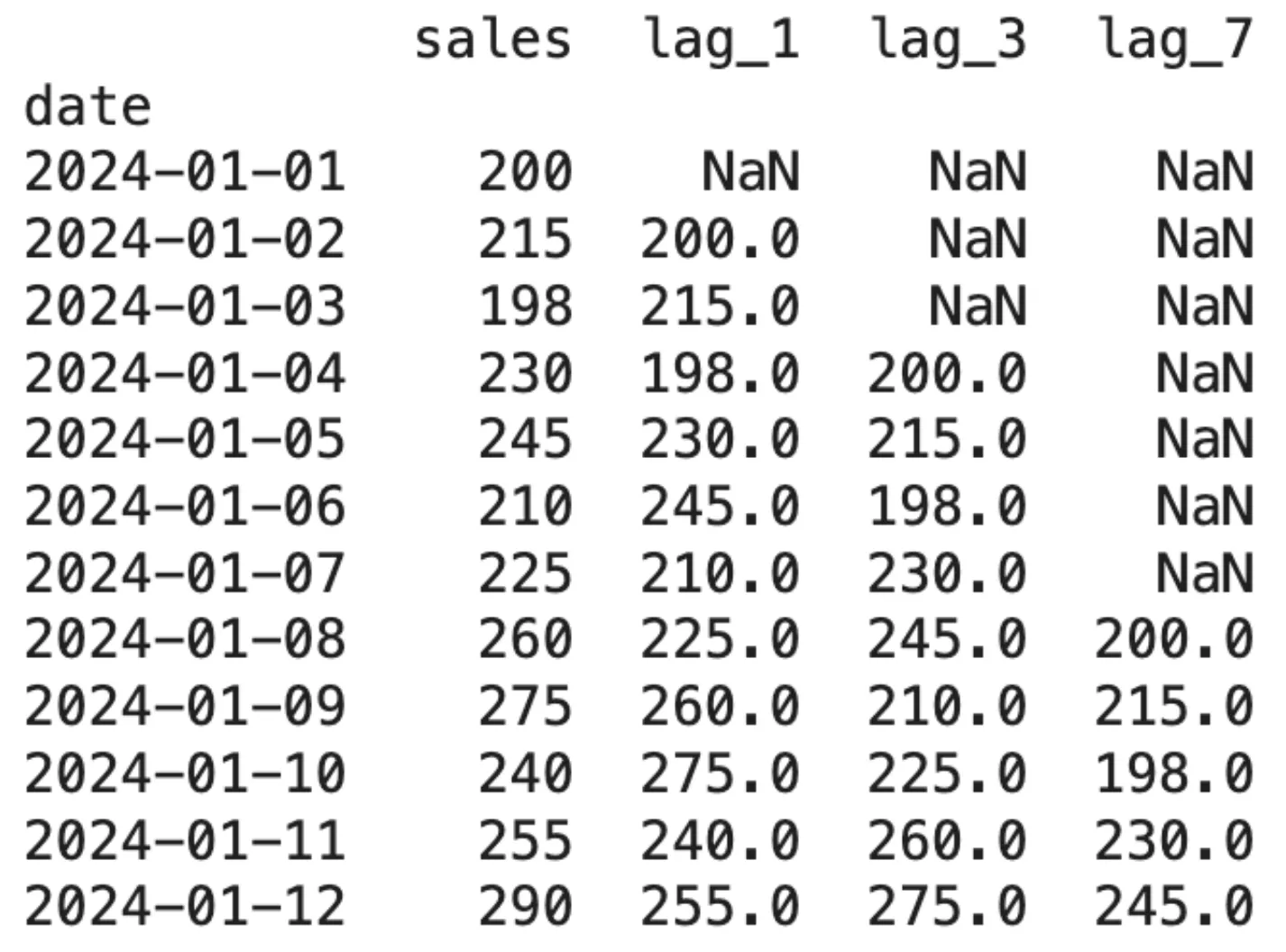

print(df.head(12))Output:

The preliminary look of NaN values demonstrates a type of knowledge loss that happens due to lagging. This issue turns into essential for figuring out the variety of lags to be created.

Selecting the Proper Lag Values

The choice course of for optimum lags calls for scientific strategies that get rid of random choice as an possibility. The next strategies have proven profitable leads to follow:

- The data of the area helps lots, like Weekly gross sales knowledge? Add lags at 7, 14, 28 days. Hourly power knowledge? Attempt 24 to 48 hours.

- Autocorrelation Operate ACF allows customers to find out which lags present vital hyperlinks to their goal variable by means of its statistical detection technique.

- The mannequin will establish which lags maintain the best significance after you full the coaching process.

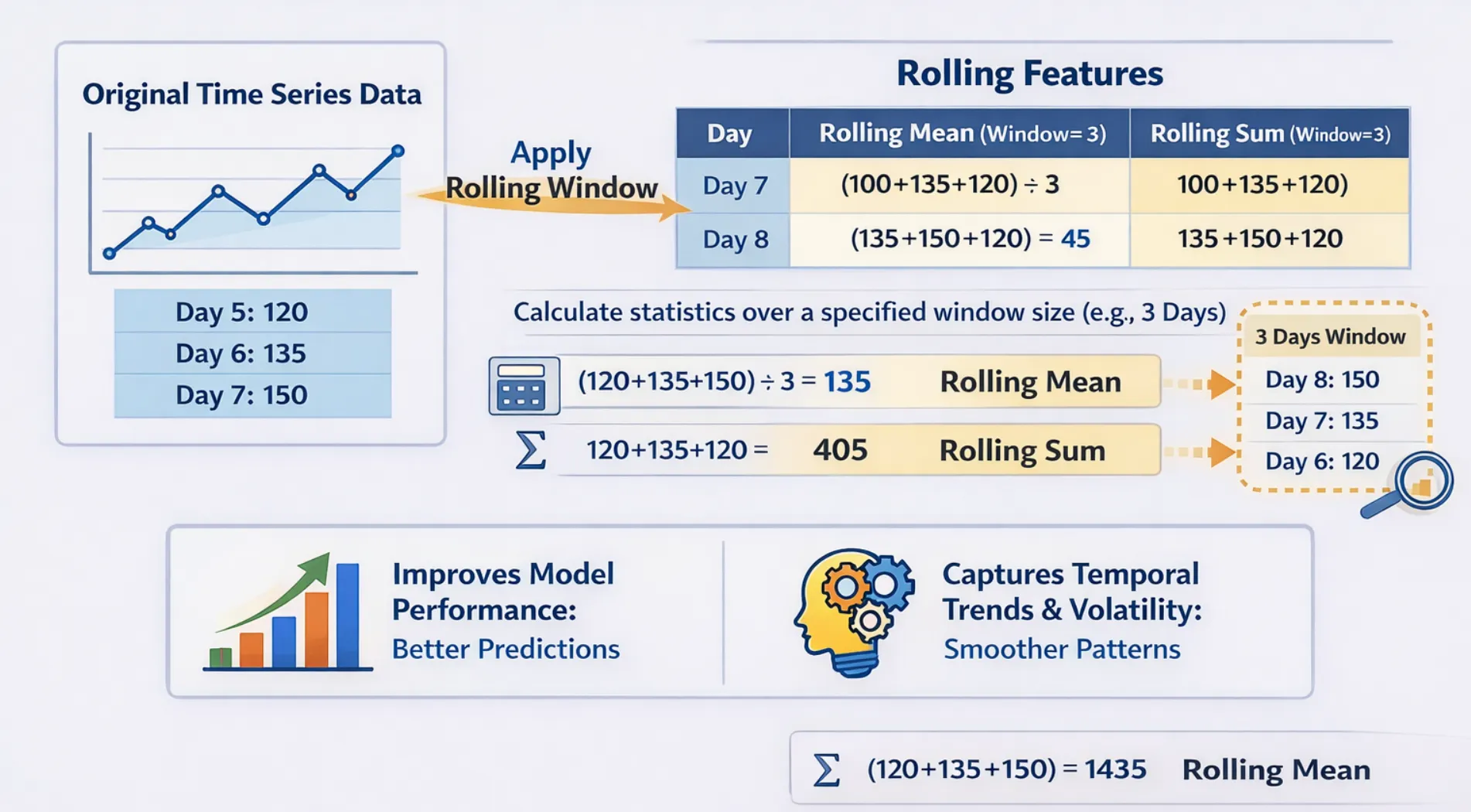

What Are Rolling (Window) Options?

The rolling options operate as window options that function by transferring by means of time to calculate variable portions. The system gives you with aggregated statistics, which embody imply, median, normal deviation, minimal, and most values for the final N durations as a substitute of exhibiting you a single previous worth.

Why Rolling Options Matter?

The next options present wonderful capabilities to carry out their designated duties:

- The method eliminates noise parts whereas it reveals the elemental progress patterns.

- The system allows customers to look at short-term worth fluctuations that happen inside particular time durations.

- The system allows customers to look at short-term worth fluctuations that happen inside particular time durations.

- The system identifies uncommon behaviour when current values transfer away from the established rolling common.

The next aggregations set up their presence as normal follow in rolling home windows:

- The commonest technique of development smoothing makes use of a rolling imply as its main technique.

- The rolling normal deviation operate calculates the diploma of variability that exists inside a specified time window.

- The rolling minimal and most features establish the best and lowest values that happen throughout an outlined time interval/interval.

- The rolling median operate gives correct outcomes for knowledge that features outliers and reveals excessive ranges of noise.

- The rolling sum operate helps monitor whole quantity or whole depend throughout time.

Implementing Rolling Options in Python

import pandas as pd

import numpy as np

np.random.seed(42)

dates = pd.date_range(begin="2024-01-01", durations=15, freq='D')

gross sales = [200, 215, 198, 230, 245, 210, 225, 260, 275, 240, 255, 290, 305, 270, 285]

df = pd.DataFrame({'date': dates, 'gross sales': gross sales})

df.set_index('date', inplace=True)

# Rolling options with window measurement of three and seven

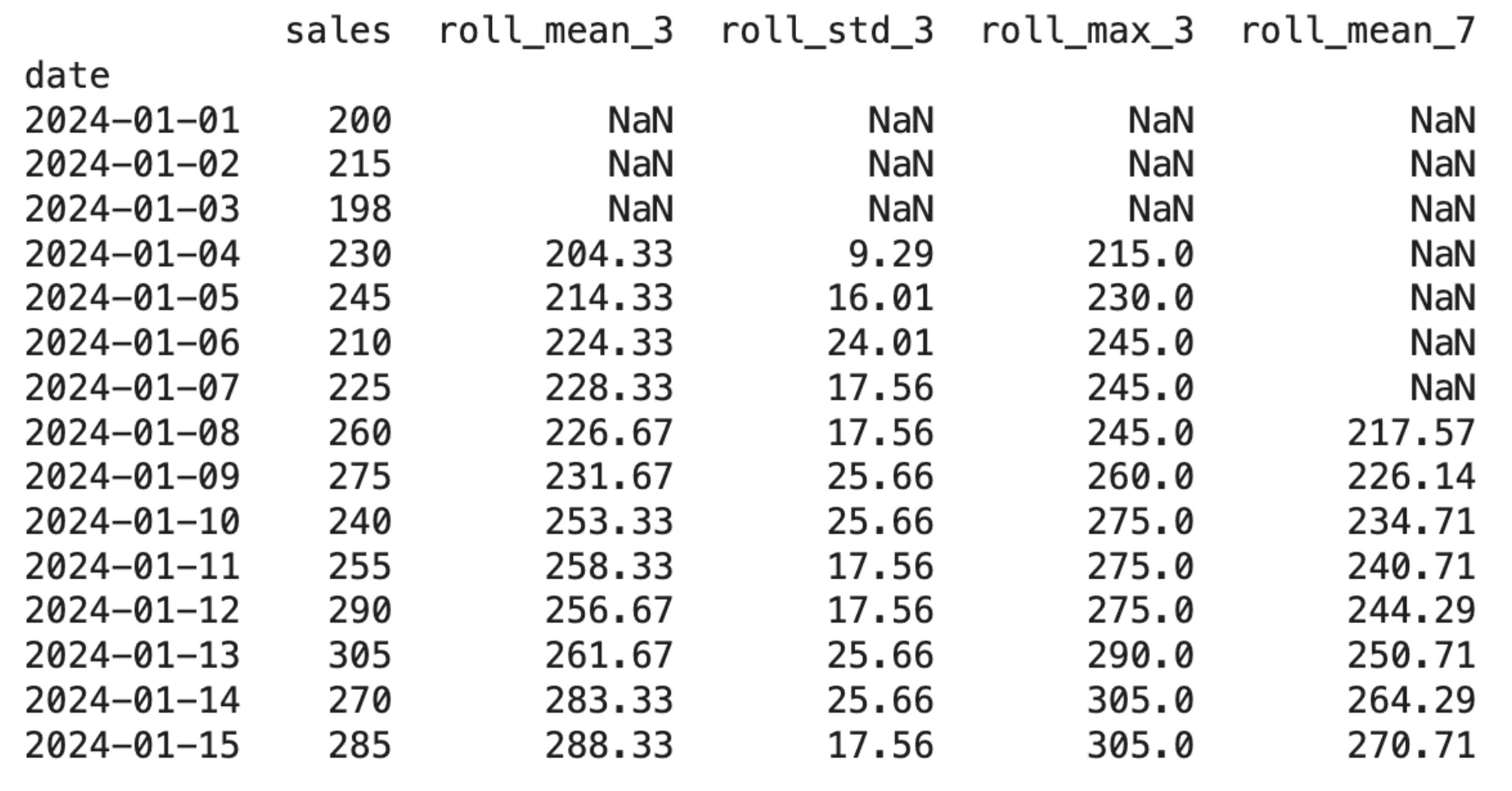

df['roll_mean_3'] = df['sales'].shift(1).rolling(window=3).imply()

df['roll_std_3'] = df['sales'].shift(1).rolling(window=3).std()

df['roll_max_3'] = df['sales'].shift(1).rolling(window=3).max()

df['roll_mean_7'] = df['sales'].shift(1).rolling(window=7).imply()

print(df.spherical(2))Output:

The .shift(1) operate have to be executed earlier than the .rolling() operate as a result of it creates a significant connection between each features. The system wants this mechanism as a result of it can create rolling calculations that rely solely on historic knowledge with out utilizing any present knowledge.

Combining Lag and Rolling Options: A Manufacturing-Prepared Instance

In precise machine studying time sequence workflows, researchers create their very own hybrid characteristic set, which incorporates each lag options and rolling options. We give you an entire characteristic engineering operate, which you should use for any undertaking.

import pandas as pd

import numpy as np

def create_time_features(df, target_col, lags=[1, 3, 7], home windows=[3, 7]):

"""

Create lag and rolling options for time sequence ML.

Parameters:

df : DataFrame with datetime index

target_col : Title of the goal column

lags : Checklist of lag durations

home windows : Checklist of rolling window sizes

Returns:

DataFrame with new options

"""

df = df.copy()

# Lag options

for lag in lags:

df[f'lag_{lag}'] = df[target_col].shift(lag)

# Rolling options (shift by 1 to keep away from leakage)

for window in home windows:

shifted = df[target_col].shift(1)

df[f'roll_mean_{window}'] = shifted.rolling(window).imply()

df[f'roll_std_{window}'] = shifted.rolling(window).std()

df[f'roll_max_{window}'] = shifted.rolling(window).max()

df[f'roll_min_{window}'] = shifted.rolling(window).min()

return df.dropna() # Drop rows with NaN from lag/rolling

# Pattern utilization

np.random.seed(0)

dates = pd.date_range('2024-01-01', durations=60, freq='D')

gross sales = 200 + np.cumsum(np.random.randn(60) * 5)

df = pd.DataFrame({'gross sales': gross sales}, index=dates)

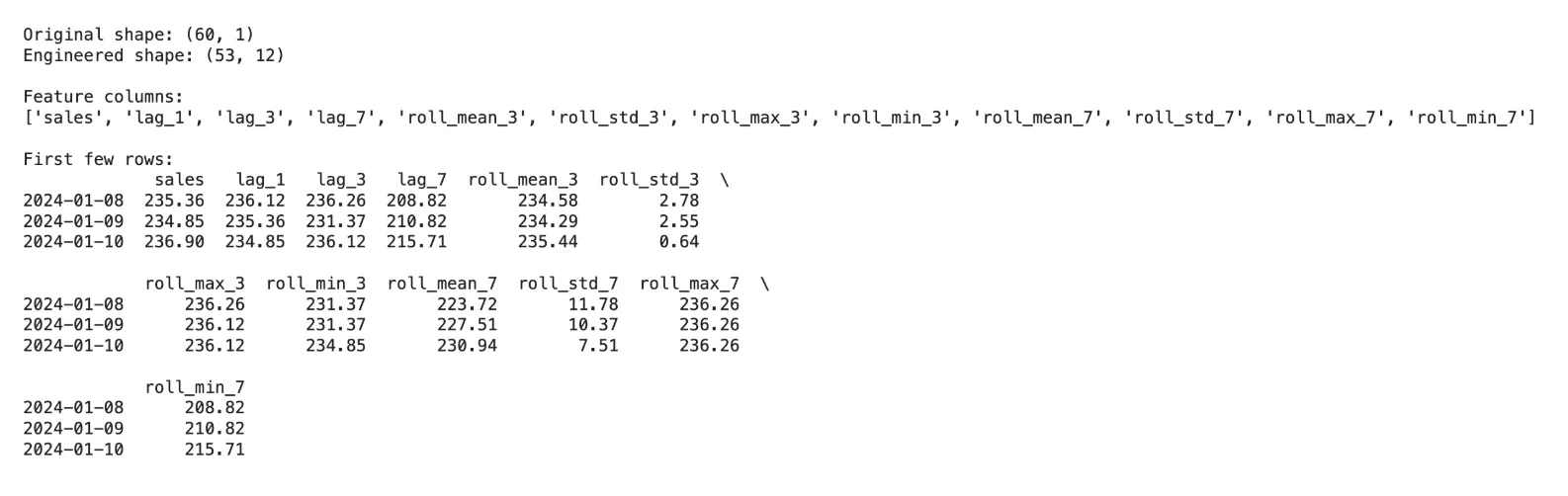

df_features = create_time_features(df, 'gross sales', lags=[1, 3, 7], home windows=[3, 7])

print(f"Authentic form: {df.form}")

print(f"Engineered form: {df_features.form}")

print(f"nFeature columns:n{checklist(df_features.columns)}")

print(f"nFirst few rows:n{df_features.head(3).spherical(2)}")Output:

Frequent Errors and Methods to Keep away from Them

Probably the most extreme error in time sequence characteristic engineering happens when knowledge leakage, which reveals upcoming knowledge to testing options, results in deceptive mannequin efficiency.

Key errors to be careful for:

- The method requires a .shift(1) command earlier than beginning the .rolling() operate. The present statement will turn into a part of the rolling window as a result of rolling requires the primary statement to be shifted.

- Knowledge loss happens by means of the addition of lags as a result of every lag creates NaN rows. The 100-row dataset will lose 30% of its knowledge as a result of 30 lags require 30 NaN rows to be created.

- The method requires separate window measurement experiments as a result of completely different traits want completely different window sizes. The method requires testing brief home windows, which vary from 3 to five, and lengthy home windows, which vary from 14 to 30.

- The manufacturing atmosphere requires you to compute rolling and lag options from precise historic knowledge, which you’ll use throughout inference time as a substitute of utilizing your coaching knowledge.

When to Use Lag vs. Rolling Options

| Use Case | Beneficial Options |

|---|---|

| Sturdy autocorrelation in knowledge | Lag options (lag-1, lag-7) |

| Noisy sign, want smoothing | Rolling imply |

| Seasonal patterns (weekly) | Lag-7, lag-14, lag-28 |

| Development detection | Rolling imply over lengthy home windows |

| Anomaly detection | Deviation from rolling imply |

| Capturing variability / threat | Rolling normal deviation, rolling vary |

Conclusion

The time sequence machine studying infrastructure makes use of lag options and rolling options as its important elements. The 2 strategies set up a pathway from unprocessed sequential knowledge to the organized knowledge format that machine studying fashions require for his or her coaching course of. The strategies turn into the best influence issue for forecasting accuracy when customers execute them with exact knowledge dealing with and window choice strategies, and their contextual understanding of the precise discipline.

The perfect half? They supply clear explanations that require minimal computing assets and performance with any machine studying mannequin. These options will profit you no matter whether or not you utilize XGBoost for demand forecasting, LSTM for anomaly detection, or linear regression for baseline fashions.

Gen AI Intern at Analytics Vidhya

Division of Laptop Science, Vellore Institute of Expertise, Vellore, India

I’m at the moment working as a Gen AI Intern at Analytics Vidhya, the place I contribute to revolutionary AI-driven options that empower companies to leverage knowledge successfully. As a final-year Laptop Science pupil at Vellore Institute of Expertise, I deliver a strong basis in software program improvement, knowledge analytics, and machine studying to my position.

Be at liberty to attach with me at [email protected]

Login to proceed studying and revel in expert-curated content material.

{kind=link}