An unpredictable H1 2025 has formed new wants for the innovation ecosystem for extra rigorously curated funding that may stand up to potential shocks to the funding panorama. We took inventory of some necessary themes prior to now six months:

- The will for power safety knowledgeable applied sciences that obtain funding with market leaders adopting more and more protectionist attitudes to fight uncertainty and geopolitical dynamics. Nations are veering away from larger danger power tech (i.e., photo voltaic PV manufacturing), with geothermal and hydrogen know-how receiving some assist, albeit at decrease ranges than earlier quarters.

_ - Infrastructure-focused functions behind funding rounds: To fulfill rising demand, there’s been an elevated emphasis on constructing out and strengthening present infrastructure, with explicit emphasis on grid applied sciences and manufacturing.

_ - Increasing alternatives in and round AI influenced cleantech growth: AI stays a major affect on which sectors preserve netting fairness funding. Power environment friendly computing, sustainable energy sources for information facilities, and applied sciences that strengthen AI’s compatibility with present power and grid infrastructure and its functions in meals safety, transportation, and manufacturing are areas of progress.

As we transfer into H2, let’s verify in on some predictions we made earlier:

Much less is Extra (Actually)

Prediction: Bigger, extra deliberate funding rounds will proceed to control the actions of the cleantech ecosystem, carrying on funding traits established late final 12 months.

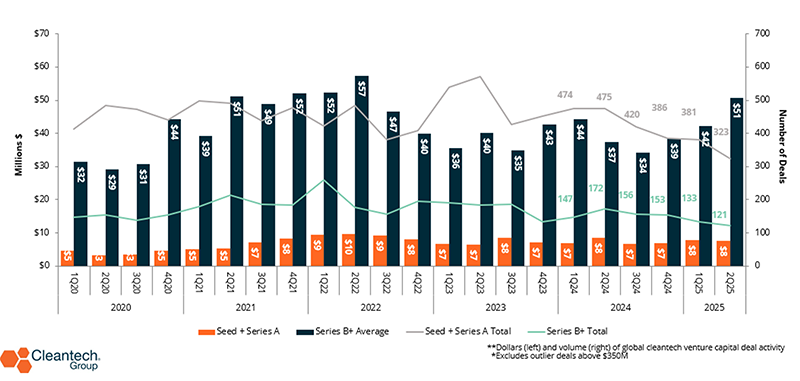

Had been we on the cash? Seems like we have been, as this funding angle was very seen within the first half of 2025, having been established on the finish of final 12 months. Later-stage ticket sizes have elevated on common by 35%. Early-stage offers are smaller and fewer frequent total.

Cleantech Funding by Stage: 2020 – 2Q 2025

The mid-stage funding ‘valley of loss of life’ continues to widen for start-ups on the Collection A stage as innovators take longer year-on-year to lift additional funding. Rising power prices, exacerbated by shifts in U.S. coverage in direction of coal-powered ‘American power dominance’, threaten the viability of cleantech growth that depends closely on materials exports and world provide chains:

- Whereas early-stage exercise in APAC has been on a gentle decline since 2024, substantial funding in tried-and-tested sectors like power environment friendly heating, air flow, and cooling (HVAC), sustainable logistics, and good livestock administration drove up common late-stage spherical measurement by 49% in H1 2025 from H2 2024.

_ - The February launch of the EU’s Omnibus simplifying sustainability reporting and disclosure supported regional curiosity in environmental monitoring. Funding peaked in Q1 by way of early-stage offers, then helped to bump Q2’s common late-stage spherical sizes by way of spacecraft designed for aerial monitoring and earth remark. House-related tech with functions in environmental monitoring gained traction in 2025, helped by EU-wide initiatives just like the European House Company’s EU House Act aimed toward strengthening regional space-related know-how growth and deployment.

_ - Sustainable mining improvements nudged up early-stage exercise in North America. Latest efforts by the Carbon Alliance push to tie mining coverage with carbon seize, with the latter being one of many few cleantech sectors that’s persevering with to obtain grant funding into this 12 months. Bilateral efforts between Canada and Mexico selling sustainable mineral useful resource governance supported some late-stage funding into AI-powered extraction/surveying know-how.

Cog within the Machine

Prediction: Industrial/company engagement will enhance in a ‘thinner’ funding surroundings.

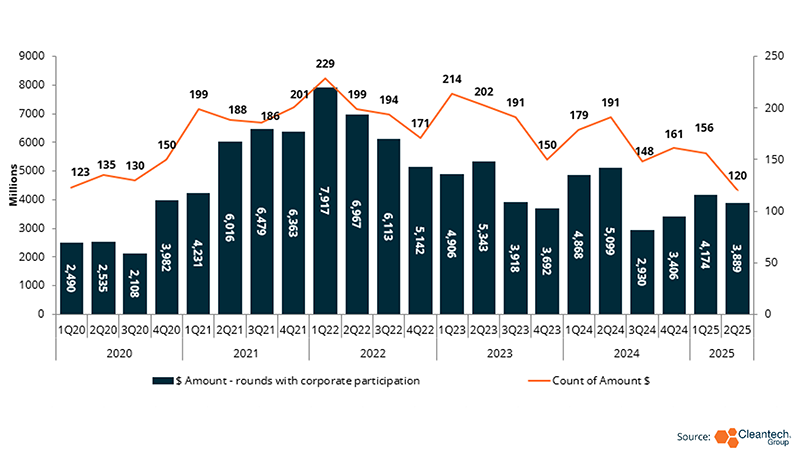

Had been we on the cash? Company participation in enterprise funding appears to have slowed down with the variety of offers with company participation falling by 9% from H2 2024 to H1 2025. Total personal investor participation decreased by 20%. H1’ s venture-backed mergers and acquisitions (M&A) add nuance to this slowdown, having maintained comparatively regular ranges since 2023. Q2 of this 12 months noticed M&A exercise focus on power networks and grid innovation, helmed by NRG Power’s $12B acquisition of CPower aimed toward growing presence and manufacturing.

Company Participation in Cleantech Funding: 2020 – 2Q 2025

Tipping the Scale

Prediction: The surge of first-of-a-kind (FOAK) applied sciences hitting the market and elevating funding in 2024 will sign stronger emphasis on scaling total.

Had been we on the cash? This 12 months’s enterprise rounds labored in direction of growing manufacturing, furthering product and know-how deployment, and dealing in direction of realizing infrastructure in a position to deal with rising power demand. An ecosystem-wide need for safety, particularly power safety, knowledgeable decision-making and capital movement throughout all areas.

Power storage, nuclear, and sustainable fuel-related FOAK initiatives and services acquired vital fairness funding in Q2 2025. Hybrid debt/fairness or debt/grant packages will assist the development of FOAKs for renewables manufacturing in Europe and the U.S. to be deployed within the subsequent 3-4 years. Conversely, large-scale photo voltaic and battery manufacturing initiatives have been cancelled having been affected by focused coverage modifications and rising prices.

- European ecosystems aligned their efforts with cleantech-related infrastructure growth, specializing in addressing regulatory challenges that forestall large-scale deployment for sectors like electrical automobile charging.

_ - Regional governments in Canada heighten give attention to vital supplies: Ontario’s proposed Invoice C-5 would streamline main infrastructure reform by quickening the authorization course of. This might encourage native traders to assist innovators decarbonizing infrastructure reform which will want such initiatives to scale up.

_ - Latin America has produced compelling FOAK initiatives and applied sciences within the final six months, together with Niko’s first digital energy plant in Mexico and Atome PLC’s ammonia-based fertilizer manufacturing facility in Paraguay, scaling options that work in direction of long-term power and meals safety.

Enjoying the Lengthy Sport

H1 2025 has proven that traders haven’t misplaced their urge for food however want to optimize their capital in a risk-filled surroundings. Alternatives with demonstrated profitability or a number of use instances are more likely to stand up to additional potential shocks to a quickly evolving panorama. Alongside safety, resiliency will assist outline the attitudes of traders and ecosystem actors by way of H2 2025:

- Corporates will discover some alternatives in M&As for power tech innovators that concentrate on elevated demand for power safety, led to by the acceleration in AI and information heart growth.

_ - With a risky public-funding surroundings, innovators at earlier growth phases will want extra constant assist from the personal sector to develop their applied sciences to a scalable product. Begin-up incubators (tutorial and personal) are effectively outfitted to fill and reap the benefits of this hole.

_ - Strategic, innovation-focused partnerships shall be key for innovators in any respect phases, from acceleration to commercialization.

{kind=link}